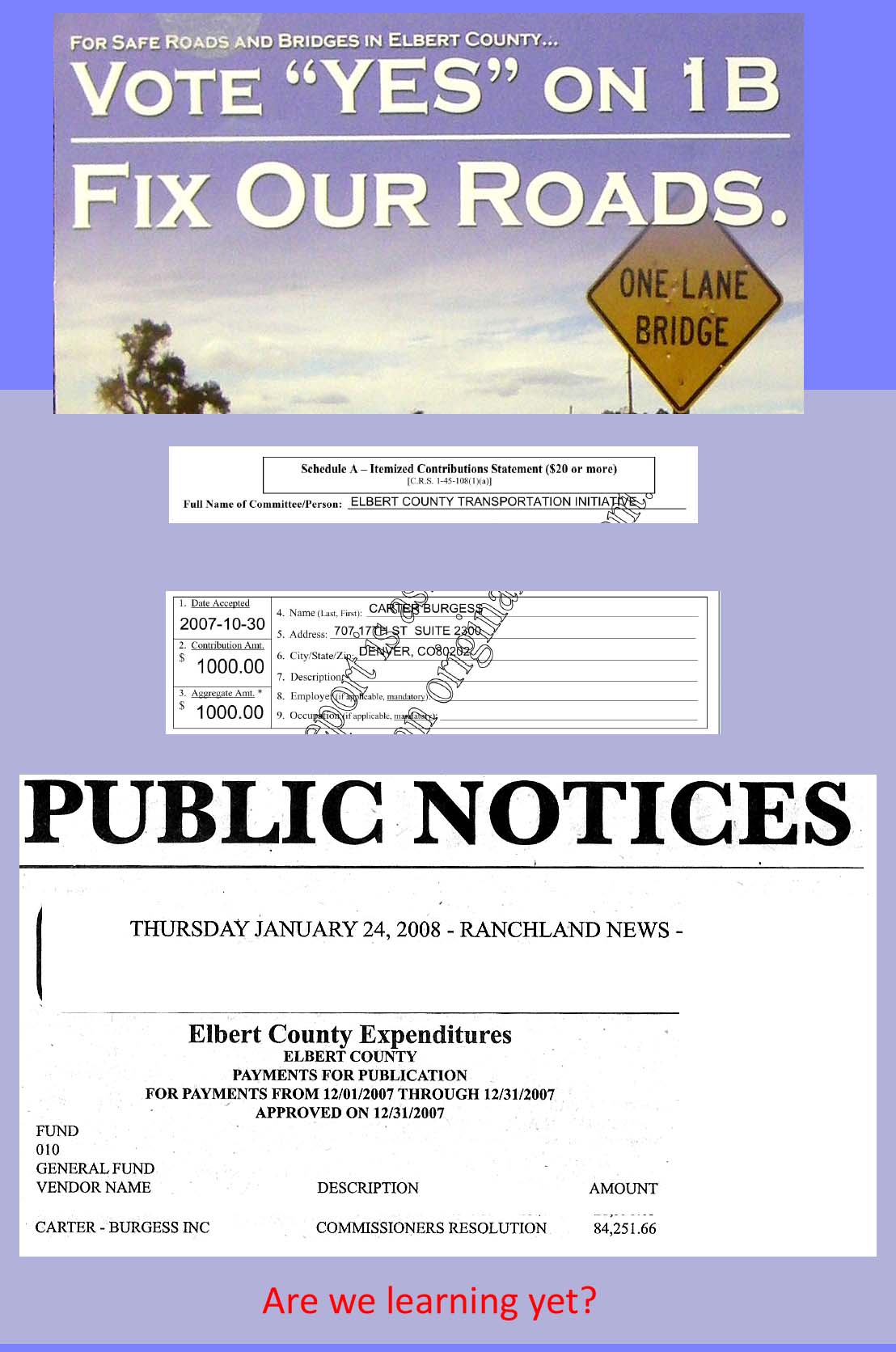

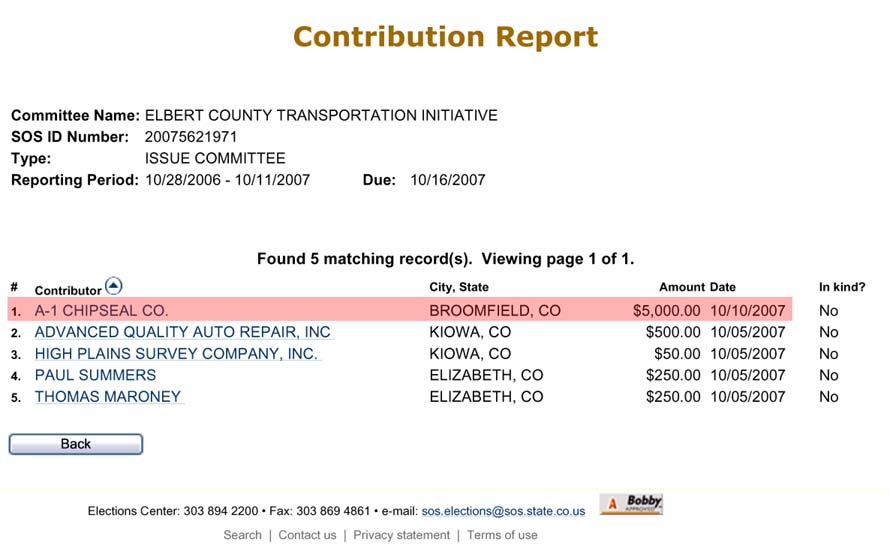

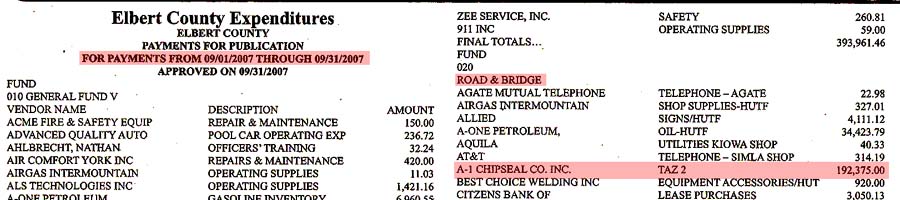

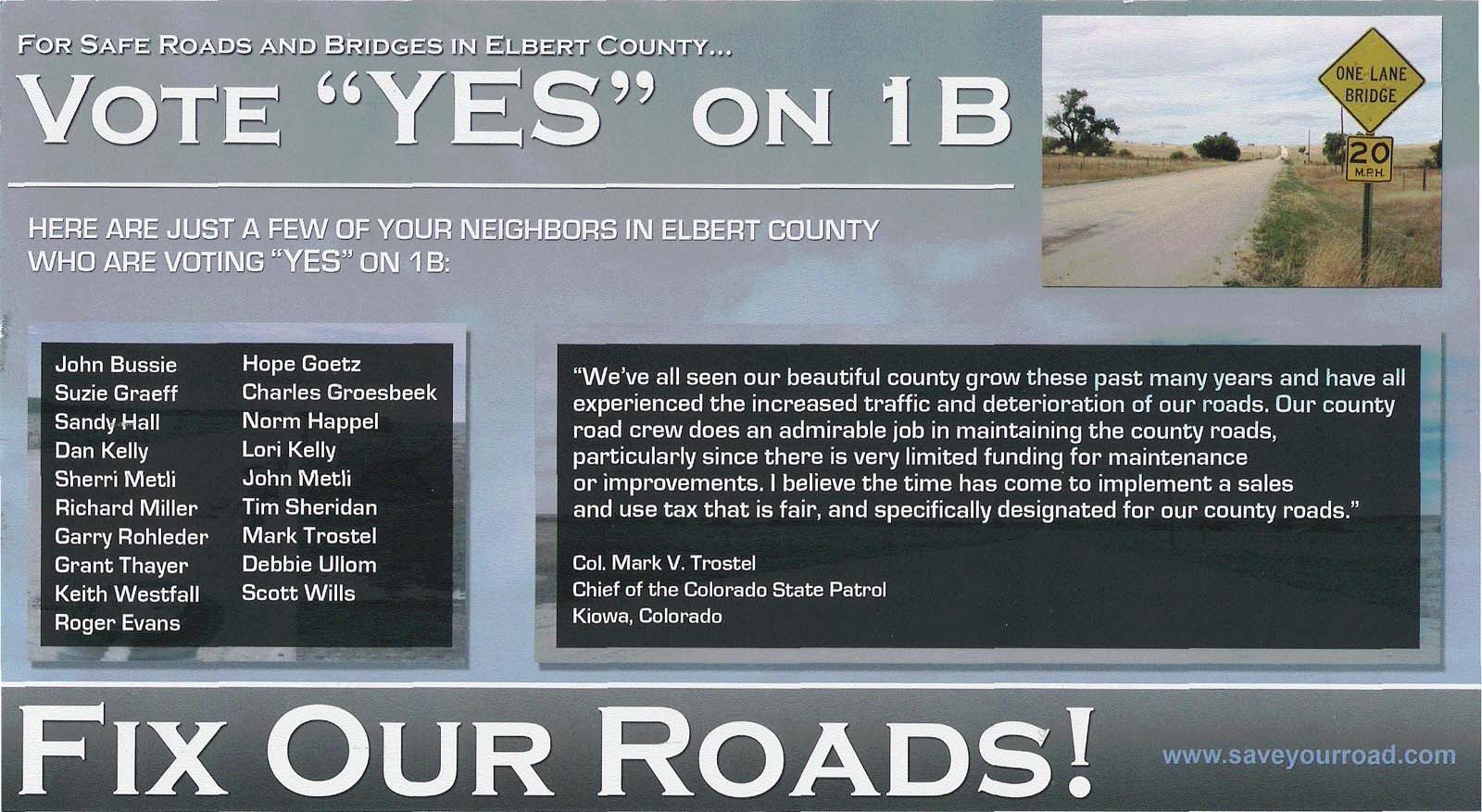

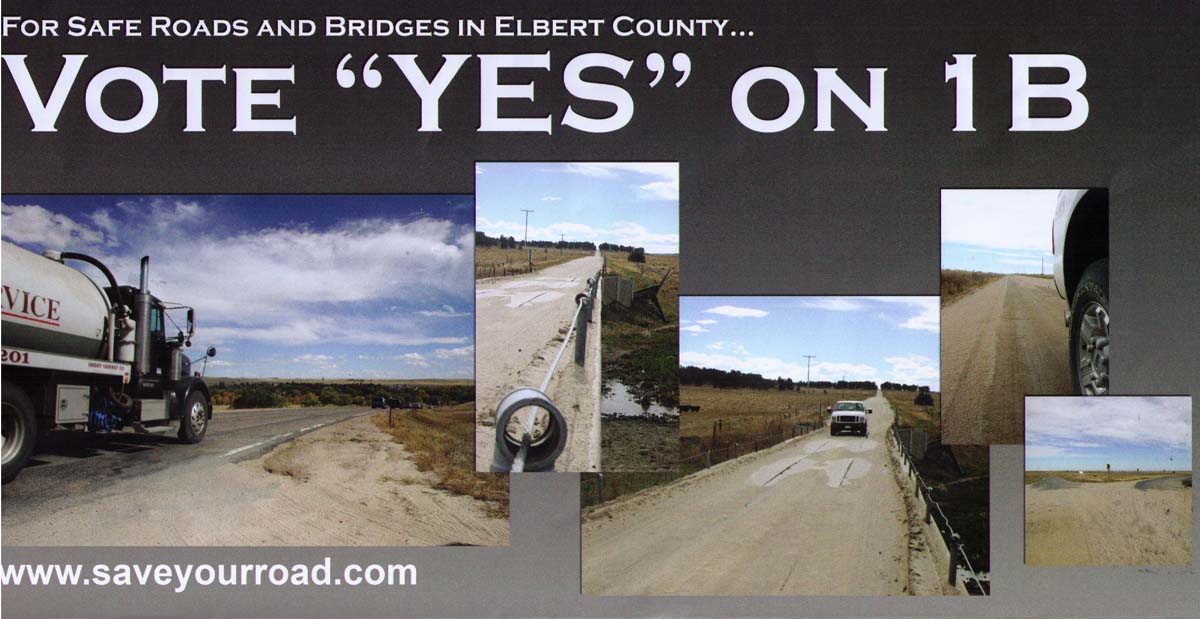

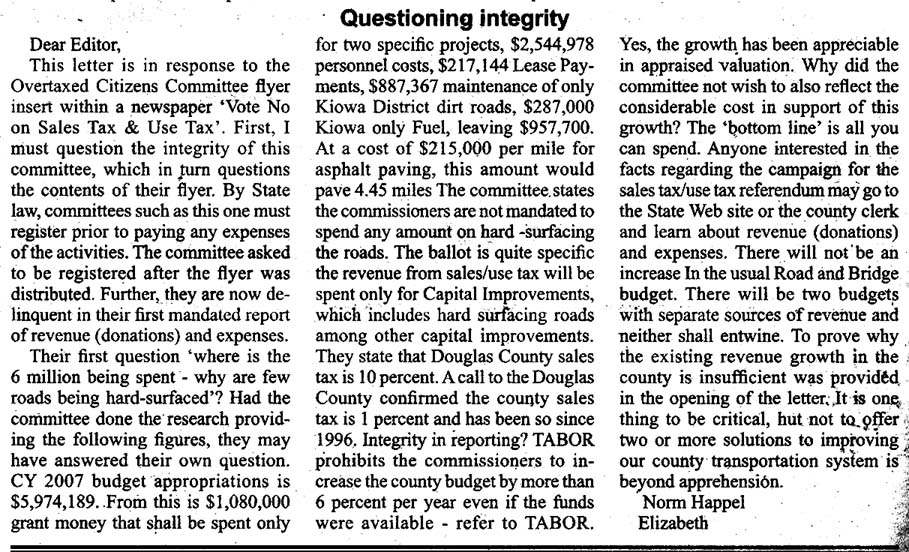

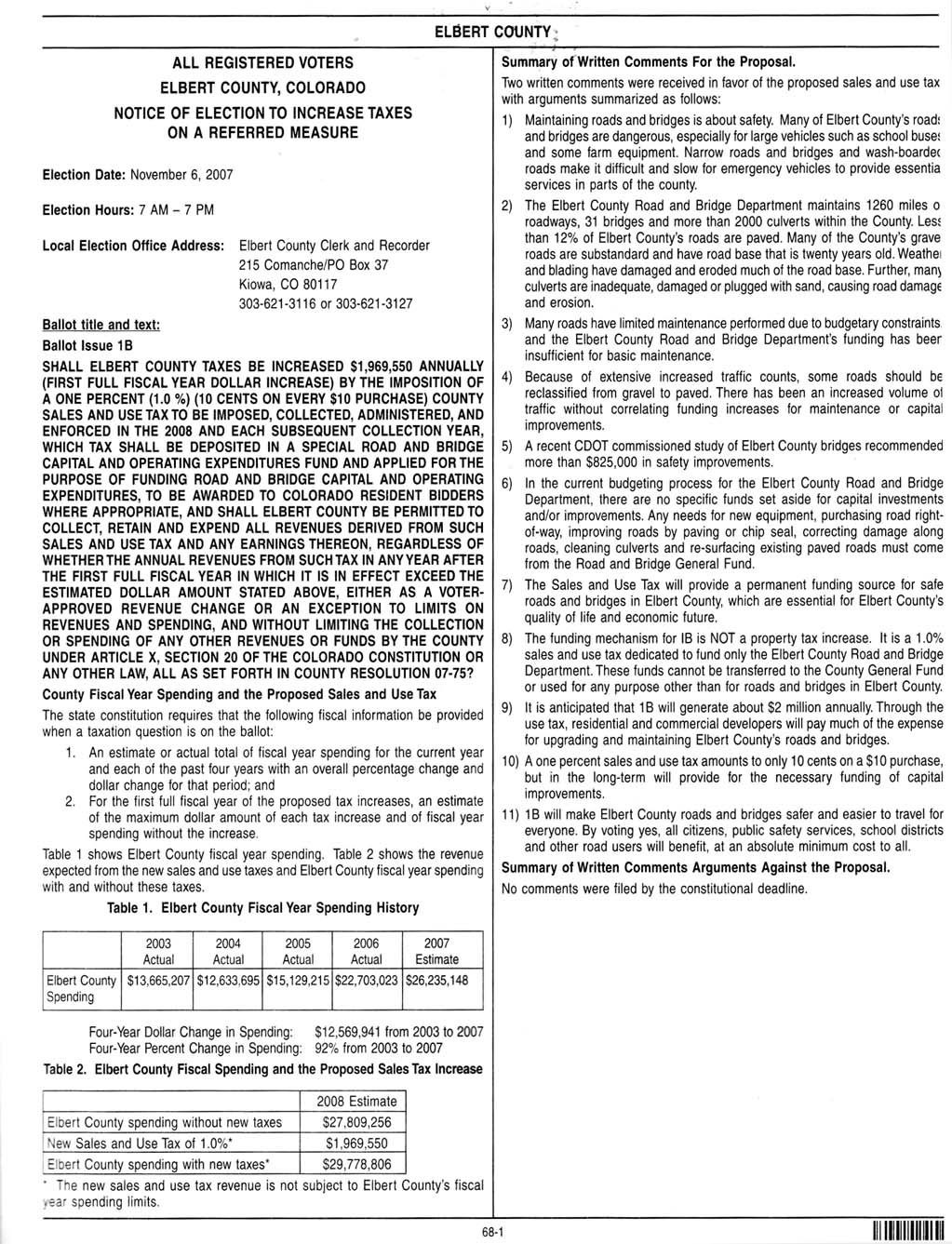

Mr. Happel’s words about the necessity for safety’s sake of fixing Elbert County road berms still ring in my ears. The Thomasson’s supported the tax too, and now resent the tax being used in the same way, almost down to the same picture (!!) as it was sold.

(click on images to enlarge)

They gave the county a blank check forever, the county did exactly what it was told to do, and now they’re whining about it. Perhaps worst of all, the chance they will learn from this expensive lesson is approximately zero.

.

.

{kind=link}

{kind=link}

{kind=link}